Introduction

This module covers basic information on maintaining books and records to comply with the requirements for registered charities.

- Purpose of maintaining books and records

- Format of the records

- Types of records

- Language of the records

- Location of the records

- Records and oversea operations

- Inadequate records

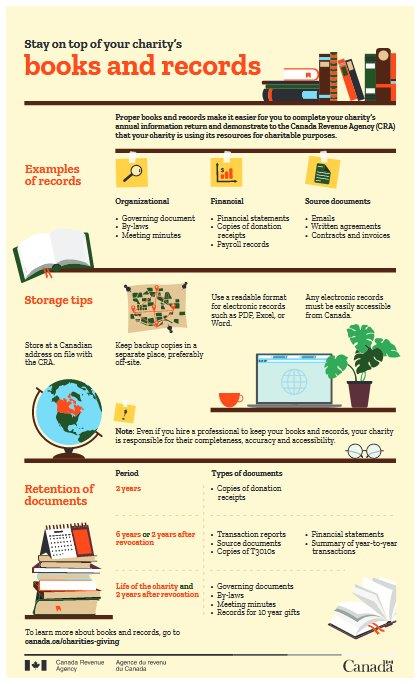

Purpose of the Records

The records should allow CRA to verify

- revenues including charitable donations received;

- that resources and expenses are used on charitable programs;

- that revenues and expenses are supported by source documents;

- that the charity’s purposes and activities continue to be charitable.

Format

Books and records can be kept in

print or electronic format

Information on the formats of books and records with emphasis on electronic records is available at: Books and Records – Format

Types of Records

According to CRA, books and records include:

- Governing documents (incorporating documents, constitution, trust document, bylaws)

- Financial statements

- Copies of official donation receipts

- Copies of T3010 annual information returns

- Written agreements and contracts

- Minutes of board/executives and staff meetings

- Annual reports

- Ledgers

- Bank statements

- Expense accounts

- Inventories

- Investment agreements

- Accountant’s working papers

- Payroll records

- Source documents or supporting documents. These include items such as invoices, vouchers, purchase orders, formal contracts, receipts, bank deposit slips, emails and other correspondence in support of transactions.

- Promotional materials

- Fundraising materials

- Other records

As a general rule, CRA does not specify the specific books and records that a charity has to keep as long as the records can verify the information that they need as stated in the page, “Purpose of the Records” .

More information can be found at: https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/keeping-records.html

Although CRA does not require you to keep more than one copy of your records, it is prudent to keep duplicate books and records in a different location.

Language

Registered charities must keep adequate books and records in:

English or French

The language used in the charitable activities does not affect the language of the books and records.

Special approval has to be granted by CRA for a charity to keep its books and records in a language other than French or English.

Location

The books and records must be physically located in Canada at the address registered with Canada Revenue Agency (CRA). This applies to both print and electronic books and records.

The address does not have to be in a business office. It could be at the board treasurer’s home as long as it is the registered address in Canada.

The address cannot be a postal box.

Responsibilities

A registered charity is responsible for properly maintaining its books and records.

If the charity contracts or hires a third party to maintain its records, the charity is still responsible for meeting the requirements.

Third parties includes accountants, bookkeepers, Internet transactions managers and application service providers.

Overseas Operations

Registered charities operating overseas must still keep adequate books and records in English or French. These books and records must be physically located in Canada.

Inadequate Records

Canada Revenue Agency may take action when a charity’s records are considered inadequate.

Actions may include:

- Issuing a requirement that adequate records be provided;

- Suspending the charity’s tax-receipting privileges;

- Revoking the charitable status of those that have not provided adequate records.

More information:

- Registered Charities Newsletter, Issue No. 26

- Keeping Records

- IC78-10R5, Books and Records Retention/Destruction

- IC05-1R1, Electronic Record Keeping

- Keeping adequate books and records (Checklist)

Notice

Information in this module is provided for general educational purposes and not as legal or accounting advice. Consult a lawyer or accountant for professional advice.

Information is accurate as of 2019.

For changes after this date, consult Canada Revenue Agency.